Remember when retirement planning involved little more than clipping bond coupons and counting on a pension? Grandpa’s biggest market‐risk decision was whether to hold his savings in 8 % CDs or 9 % CDs.

Then, in the 1970s, the 401(k) was born, and with it came a seismic shift in how Americans approached retirement. As pensions faded into history, investors were suddenly thrust into the driver’s seat of their own financial futures. The industry’s solution? A “set it and forget it” approach built around the 60/40 portfolio – 60% stocks for growth, 40% bonds for safety.

The result? Pre-retirees are often far more exposed to stock-market volatility than they bargained for. And after 2022’s one-two punch—both stocks and bonds falling together—many investors learned the hard way that “diversified” doesn’t always mean “protected.”

So, where can you find growth and a good night’s sleep? Increasingly, the answer lies outside the public markets’ echo chamber. Think private-equity deals that don’t trade tick-by-tick, venture-capital funds backing tomorrow’s disruptors, hedge funds built to profit in both boom and bust, or infrastructure projects paying steady cash flows whether the S&P is partying or pouting. These alternative assets march to different drummers—and that uncorrelated beat is precisely the point.

In short, the challenge isn’t just beating volatility; it’s finding assets that care about different things entirely. If you want to position yourself away from stock market volatility, it may be time to widen the opportunity set before the next roller-coaster drop. Let’s dig into what these alternative buckets are, why they matter right now, and how they could fit into a sturdier, post-pension portfolio.

What Are “Alternative Assets,” Anyway?

Alternative asset is basically a catch-all phrase for anything you invest in that isn’t a publicly traded stock, bond, or cash instrument. If it’s not on the New York Stock Exchange or similar, it falls into this bucket.

So what does that include? Potentially a wide world of investments, from the mundane to the ultra-creative. Here are just a few examples of alternative assets that you might even already own or have considered.

Private Equity

Private equity involves funds or investors directly buying entire private companies—often established businesses—that aren’t listed on public stock exchanges. The goal is typically to improve operations, expand the business, or prepare it for an eventual profitable sale or initial public offering (IPO). Private equity tends to offer higher potential returns compared to traditional stocks, partly because investors are compensated for tying up their money for several years and taking on more operational risk. This long-term nature means your investment is usually illiquid for quite a while (though probably not as long as your funds tied up in an IRA or 401(k)), but it also means private equity returns aren’t typically subject to the daily volatility of the public stock market.

Venture Capital

Venture capital (VC) is a specialized subset of private equity that invests in early-stage companies—often startups or innovative ventures—that show potential for rapid growth but lack an established track record. Unlike traditional private equity, venture capital is higher risk and potentially higher reward, as many startup investments fail outright, while the few successful companies may provide outsized returns. Venture capital typically requires even more patience and risk tolerance, as investments usually remain illiquid for as much as a decade. The payoff, however, can be significant if investors identify and support the next breakthrough technology or transformative industry leader.

Hedge Funds

Hedge funds are pooled investment vehicles run by professional managers who use complex strategies designed to deliver returns independent of the broader stock and bond markets. Strategies vary widely: some hedge funds might short-sell stocks, bet on currency movements, engage in arbitrage strategies, or use derivatives to hedge risk. Unlike mutual funds, hedge funds typically require larger minimum investments and may charge higher fees. However, their appeal lies in their flexibility and ability to potentially generate positive returns even in down markets.

Infrastructure Funds

Infrastructure funds invest in projects and assets that provide essential public or private services, like roads, bridges, airports, telecommunications towers, renewable energy plants, or utilities. These investments often generate steady cash flows from user fees or contracts, frequently indexed to inflation, providing a stable and predictable source of income. Infrastructure investments are usually less correlated with equity market movements because their revenue depends more on consistent demand than economic cycles.

Other honorable mentions include:

- Real Estate & REITs: Real estate has been the retirement backbone for many through rental properties or house flipping. It’s tangible, it’s often a good inflation hedge (more on that later), and it doesn’t always move in sync with the stock market.

- Cryptocurrency: Crypto is as “alternative” as it gets – digital assets powered by blockchain technology. Extremely volatile (your $100 can turn into $200 or $20 in a blink), but often independent from traditional market drivers.

- Collectibles and Others: Ever watch Antiques Roadshow? Art, classic cars, rare whiskey, baseball cards – if it’s an asset with value that isn’t a stock or bond, it’s an “alternative investment”.

In short, alternative assets can be almost anything outside the Wall Street mainstream. The key thing is that they’re not your typical publicly traded securities. And because of that, they often march to a different beat than stocks and bonds.

Why Are Alternatives Suddenly So Relevant?

The logic surrounding alternative assets lately comes down to a few key reasons:

Diversification & Lower Correlation

One of the golden rules of investing is “don’t put all your eggs in one basket.” Alternatives are like new baskets for your eggs. Many alternative assets have a low or even negative correlation to stocks and bonds, meaning they don’t all crash at once. For example, gold often zigs when stocks zag (gold has had near-zero or slightly negative correlation with equities historically).

Real estate or private equity might chug along based on local market cycles or specific business growth, relatively independent of the S&P 500. The idea is that adding some of these to your mix can smooth out the ride. You’ve seen the charts – in 2022, both stocks and bonds fell together, leaving a traditional portfolio with nowhere to hide. Alternatives offer a new place to hide (or even profit) when conventional markets falter.

Potential for Higher Returns

Many alternatives aim to deliver higher returns than plain-vanilla stocks or bonds (though they might do it with higher risk – nothing’s free, as I’ll remind you in a second). Private equity is a poster child here. Historically, private equity funds have outperformed the stock market over the long term. In fact, over the past couple of decades, the average annual return for U.S. private equity was around 14%, compared to roughly 10% for the S&P 500. As you can see below, private equity (orange bars) beat the S&P 500 (blue bars) in each period from 5-year to 20-year averages:

Private Equity vs. S&P 500: Historical Returns

Source: fsinvestments.com.

An Inflation Hedge

Remember how I mentioned Grandpa’s bond coupons? One thing he never worried about much was inflation – his pension and bonds had cost-of-living adjustments and high fixed rates. Today, with inflation periodically rearing its ugly head, some alternative assets can help hedge against inflation. Real assets like real estate, infrastructure, or commodities (think gold, oil, or even farmland) tend to rise in value when prices in general rise.

The Erosion of Purchasing Power Over Time

For example, landlords can raise rents in inflationary times (helping real estate income keep pace with inflation), and precious metals have historically served as a store of value when paper money loses purchasing power. If you’re worried that your dollars buy less each year (hello, $7 carton of eggs), having some investments that float up with the cost of living can be a relief.

Alternative Income Streams

With bond yields not as profitable as they once were, people approaching retirement are hunting for yield. Some alternatives can provide income streams, often higher (though less certain) than bonds. Real estate rentals, private credit funds, or even dividend-paying infrastructure projects can throw off regular income. For instance, private credit (essentially playing banker to companies) can offer pretty attractive interest payments in today’s. It’s all about finding income beyond the usual suspects of Treasury bonds and bank CDs.

Exclusive Opportunities & Personal Interests

This one is more intangible, but alternatives can be fun and fulfilling in a way traditional investing isn’t. Ever feel like the stock market is just numbers on a screen? Alternatives let you invest in real things – a startup making a product you believe in, an apartment building down the road, or a piece of artwork you can hang on the wall. There’s a certain satisfaction in having part of your portfolio in something you can touch or that resonates with you personally.

Plus, some opportunities are only accessible in the private market. The number of publicly traded companies has shrunk over the last few decades, while private startups have exploded in number. By dipping into alternatives, you’re accessing a bigger universe of investments than just the stock market’s offerings.

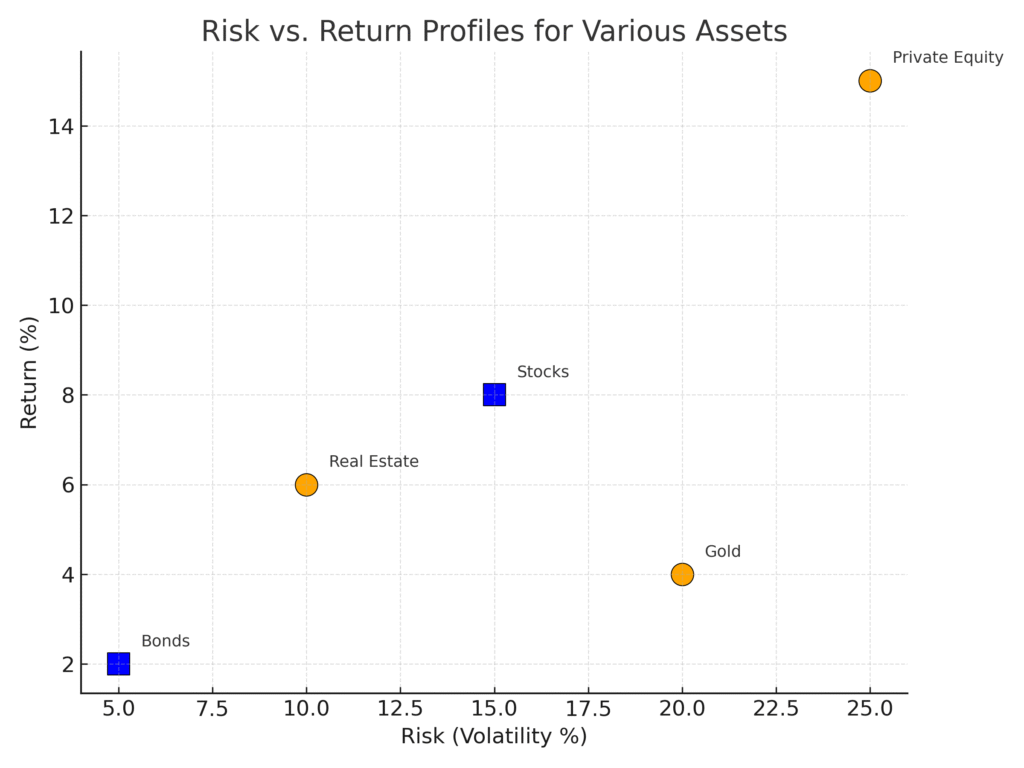

Balancing Act: Understanding the Risk/Reward Trade-Off

If an investment promises higher returns, chances are it could dish out higher losses or volatility too. This is true of stocks vs. bonds (stocks swing more and have higher long-run returns; bonds are steadier but generally have a lower return), and it’s true of alternatives as well.

Alternatives often occupy different spots on the risk/reward map than your standard stocks or bonds. Private equity, for instance, can have higher ups and downs than publicly traded stocks – it’s not unusual for a private investment to be valued 20% higher one year and 15% lower the next before a big payoff when the company goes public or gets bought. Real estate might not see wild daily swings like stocks do (your house doesn’t price itself to the second), but it can go through multi-year booms and busts. And crypto… well, anyone who’s watched Bitcoin knows that rollercoaster is not for the faint of heart.

Smoother Sailing: Diversification and Correlation Benefits

One of the biggest advantages of adding alternative assets is improved diversification. Classic finance theory (and common sense) says a well-diversified portfolio can achieve the same return with lower risk than a concentrated one. How? By mixing assets that don’t all move together. Correlation is the term we use – a measure of how tightly assets move in sync. A correlation of 1.0 means two assets are twins, moving up and down together; 0 means they dance to completely different tunes; negative means when one goes up, the other tends to go down.

Below is a chart of how different assets correlate with the stock market:

Asset Correlation with U.S. Stock Market (S&P 500)

The goal for a pre-retiree’s portfolio is usually to reduce the bumps without killing the returns. Alternatives can help do that. For instance, imagine a rough year where stocks tumble 20%. If you also hold, say, private real estate or infrastructure investments that maybe only dip a little (or even gain a bit because rent incomes kept coming), your overall portfolio won’t be down as badly. Or if inflation flares up and hurts stock valuations, maybe your gold or commodity holdings soar, offsetting some pain.

It’s worth noting that correlation patterns can change over time. There have been moments when, say, real estate and stocks both fell together or when crypto plunged alongside tech stocks. That’s why you want multiple types of alternatives – some gold, some real estate, some private equity, etc. – to cover different scenarios.

Bringing It All Together

The goal is a well-rounded retirement portfolio. For a lot of pre-retirees, that still means the bulk in reliable, time-tested holdings (blue-chip stocks, quality bonds, etc.), but potentially with an allocation – maybe 10%, 15%, 20% – in alternatives to give you an extra edge and safety net. It’s about broadening the opportunity set while keeping an eye on risk. As J.P. Morgan’s analysts noted, with stocks looking expensive and bonds yielding just so-so, alternatives like private equity, private credit, and real assets can boost long-term returns and even reduce volatility in a portfolio.

I’m always up for a down-to-earth chat about your financial goals and how alternative assets might play a role in getting you there. It’s not about jumping on bandwagons or taking unnecessary risks; it’s about crafting a resilient plan tailored to you. So, let’s talk! Click the button below to schedule a portfolio review with me.